Nobody Owns Pricing at Your Company. You’ve Decided To. Now What?

Your Dilemma

You’re the Director of Finance at a regional building products manufacturer. Doors, windows, siding, maybe some fixtures. The sales teams run quotes in Excel. Each rep has “their accounts” and “their pricing.” A pricing meeting at your company is what happens when somebody walks into your office and says they need to increase a discount by 20% to hold a national account.

You’re not the pricing person. Your company doesn’t have one. But you know things often are not adding up, you’ve seen quarter-end margin slippage chalked up to “mix” three quarters running, and so you’ve quietly decided that someone needs to start treating this like a real process, a critical capability. Apparently that someone is you.

Here’s the good news: You don’t need to hire a whole pricing team. You need three things, in this order:

- A single source of truth for what’s actually being charged.

- One person who can say no.

- A rhythm for reviewing the gap between list and pocket.

That’s the whole starter kit. The rest of this post is what each one looks like when you don’t have a mandate, a budget, or a title, and how to put it in place without quitting your day job.

(Quick aside: if you’ve read an earlier piece in this series on who actually owns pricing, this is the follow-up. Nobody owns pricing at your company because responsibility is fragmented and distributed, not because the people are bad. The three steps below are how you fix this.)

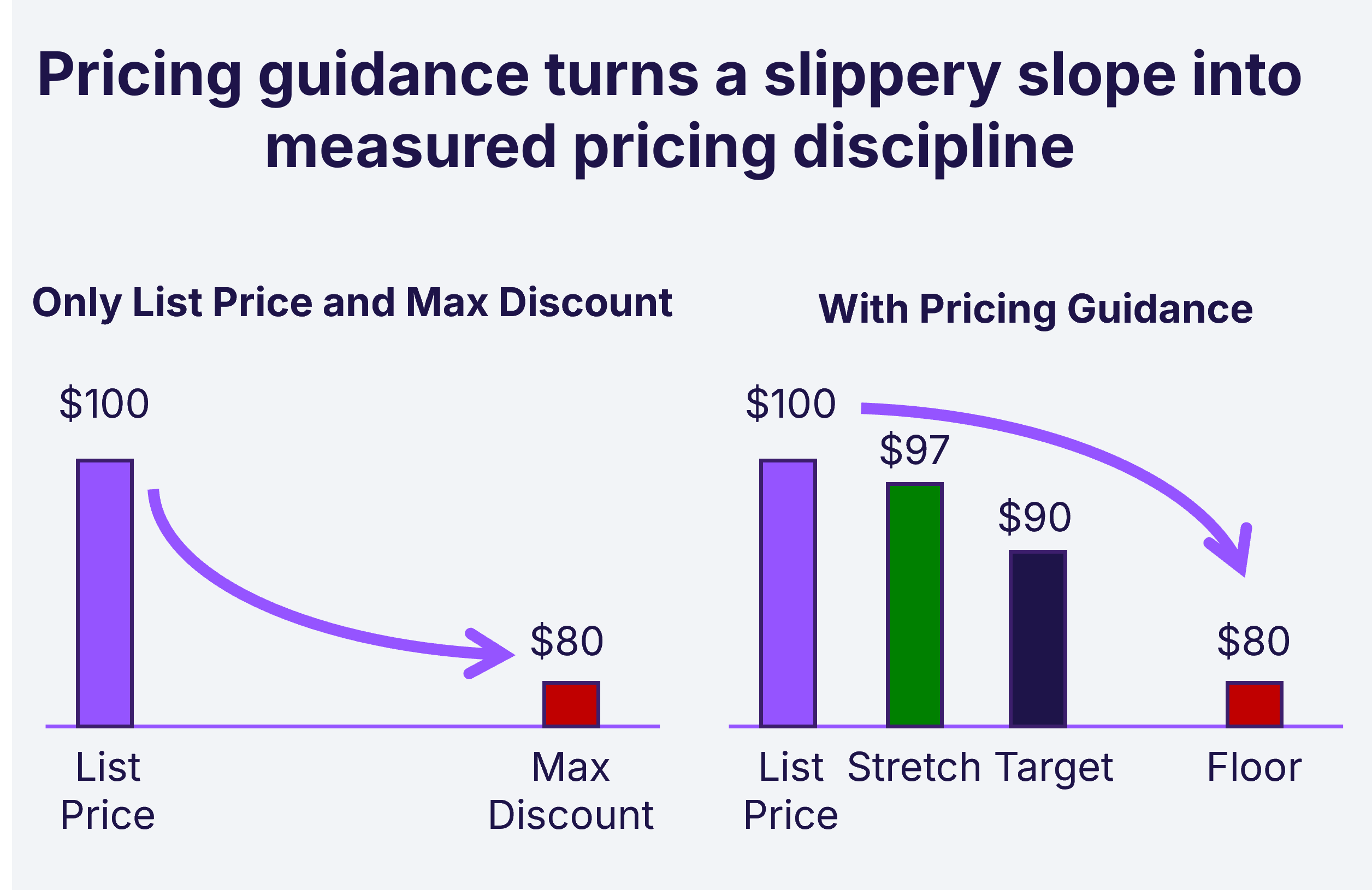

1. Build a single source of truth for what you actually charge

Set the price book aside for a minute. The price book is great, but it’s really just filled with good intentions, and you know where the road paved with good intentions goes, right? What you need is the “pocket price”: the invoiced price or revenue minus those frequently overlooked off-invoice deduction (rebates, freight absorption, payment terms, claims, returns, allowances)… not at a broad rolled-up average level… at a customer + product level, on every invoice. What you are really collecting from your customers.

The data lives in three places:

- Invoice line items in your ERP (your IT department may already have this in a data warehouse)

- Off-invoice deductions in AR/AP, finance accruals, trade marketing, and freight settlements

- Customer-specific terms in SPAs and contract files (often in someone’s email)

You don’t need a big expensive software solution, nor expensive strategy consultants. You need access and one or two allies willing to share data. Start with your top 20 customers. Spread the off-invoice adjustments down to the transaction level. Plot the distribution of pocket price by SKU for each.

The shape of that distribution will surprise you. It almost always does. (For the longer version of why, an earlier piece in this series on the Price Waterfall is the primer.)

Why this step first: without ground truth, every discount conversation is “he said / she said” and the loudest voice wins. With it, the conversation gets quieter and more accurate almost immediately.

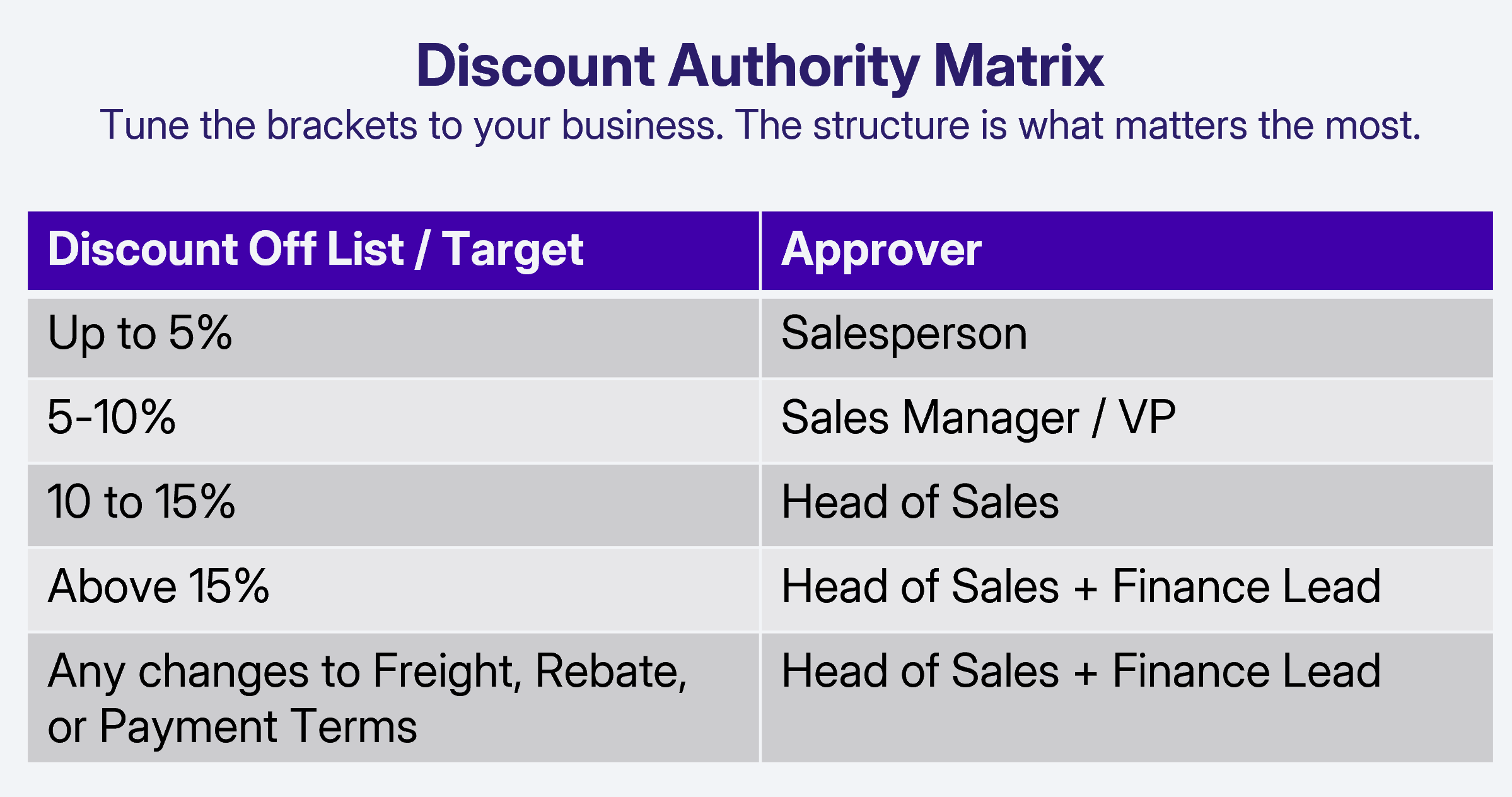

2. Name one person who can say “no”

The most common failure in distributed pricing is a missing no, not a missing strategy. When every sales rep can grant a discount, no finance person is stopping anyone, and the pricing committee meets quarterly to admire last quarter’s damage, you have a discounting culture rather than a pricing function.

You need a discount authority matrix. It does not need to be elegant. It needs to exist.

Tune the brackets to your business. The structure is what matters.

The hard part is not the table. It is naming the one person at the top who will say no when the deal feels needed but the economics don’t work. In a regional building products manufacturer that person is usually the Head of Sales, not the Director of Finance. Get that person on your side and let them have the authority. You are doing the analysis. They are doing the deciding. Both roles matter.

Expect some noise for a couple months. Reps will push back. A couple of accounts will (allegedly) threaten to leave. Most of the threats are bluffs. By the end of the quarter the matrix has more credibility than you do, which is exactly what you want.

(Next week’s article will go deeper on governance. For now, all you need is the matrix and the named person.)

3. Set a rhythm for reviewing the gap between list and pocket

Thirty minutes a month. Same calendar slot. Same five people: the named no, a sales rep, a finance partner, an operations or supply representative, and you.

The deliverable is one page. Pocket price distribution for the top 20 customers and the top 20 SKUs, this month versus last month and last quarter.

Three questions get asked:

- Where did pocket price slip the most this month, and why?

- Where did we hold a line we wouldn’t have held three months ago?

- What deal next month is going to test us, and what is the plan?

That’s it. No slides. No prep meeting for this meeting. Thirty minutes.

The rhythm is the strategy. Pricing usually breaks down because nobody is watching closely enough to notice the slippage in time to act. Source of truth gives you the data. The named no gives you the authority. The monthly rhythm turns both into a habit. Together they form the smallest possible pricing function that does real work.

Why this order

Source of truth first, because without it every conversation about discounts is opinion versus opinion.

Named no second, because authority without data is bureaucracy, and the no person needs ground truth in hand when they say no.

Rhythm third, because the first two are events, and pricing only changes outcomes when it becomes a habit.

This order is also politically defensible inside your company. You can sell step 1 to your CFO as a finance project. You can sell step 2 to your Head of Sales as a way to protect their best reps from getting cornered by their worst accounts. You can sell step 3 to your CEO as a thirty-minute monthly investment that produces a one-page dashboard. Each step buys you the next one.

What this looks like 90 days in

For a regional building products manufacturer doing $100M in annual revenue, the picture after one quarter typically looks like this:

- One workbook or platform view that shows pocket price by customer and SKU for the top 80% of revenue

- A one-page discount authority matrix that is actually used (not aspirational)

- One thirty-minute monthly review on the calendar, with attendance

- For the deals you can affect in these first 90 days, many companies see between 1% and 3% of revenue as additional price realization. And the beauty of that extra value? It’s 100% pure profit. A 1% increase in realized price would yield about 10% increase in profit. These gains come from declining to give away margin you didn’t realize you were giving, not from raising list.

These are not aspirational ranges. They are what McKinsey, BCG, and Revomo’s own client work consistently produce from this exact starter kit when a distributed-ownership company puts the three pieces in place. The recovery was always there. You just couldn’t see it, name it, or hold the line on it.

(And the political capital you build by saying no in a disciplined way? That is the start of the actual pricing function your company will eventually have. Probably with your name on it, if you want it.)

Where to start tomorrow

The smallest possible first step: pull last quarter’s invoices and credit memos for your top 10 customers. Spread the off-invoice items down to transactions. Plot pocket price by customer. Don’t share the chart yet. Just look at it.

You’ll know what to do next.

Pro Tip: Revomo is built to make step 1, the single source of truth, incredibly easy. We pull your transactions, rebates, freight absorption, payment terms, and adjustments into one pocket-price-aware view in days, not months. If you’ve quietly decided you’re the one to start this at your company, we’d be glad to compare notes. The first look is on us.

.avif)

in your inbox every week

in your inbox every week